Australia’s retirement system has undergone a significant transformation – shifting away from rigid age limits and towards more flexible, lifestyle-driven choices. While there’s no longer a compulsory retirement age, your eligibility for the Age Pension and superannuation access really is what determines when you can afford to retire comfortably.

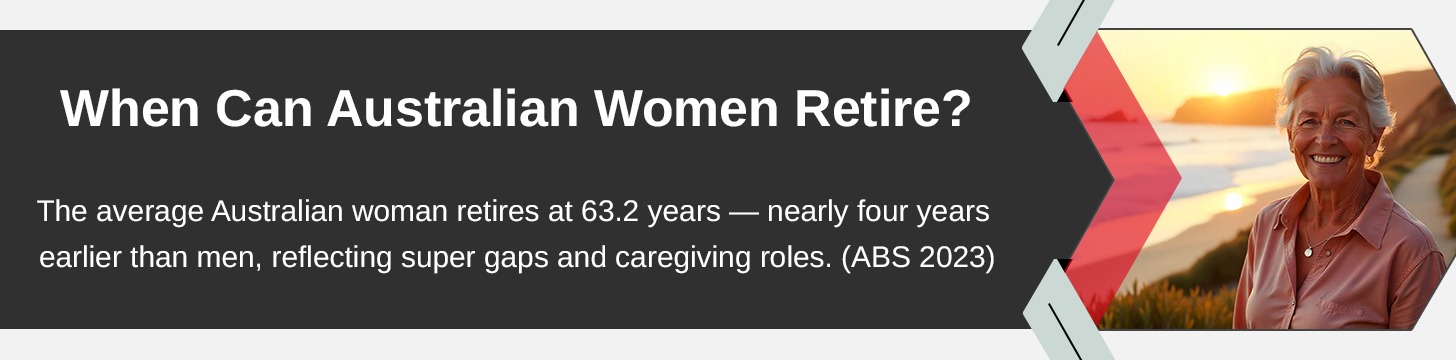

According to the Australian Bureau of Statistics (ABS), the average age at which Australians retire is 57.3 years, but the age they actually plan to retire is around 65.4 years. Women tend to retire earlier than men, largely because of family care responsibilities and earning lower salaries throughout their lives.

Below we break down everything you need to know about retirement ages, pension eligibility, superannuation access, and financial planning for a stress-free retirement.

What Age Can a Woman Retire in Australia?

There is no set age at which women have to retire in Australia – its entirely up to them. However, there are some government and financial thresholds that can give you a better idea when retirement is going to be a viable option for you:

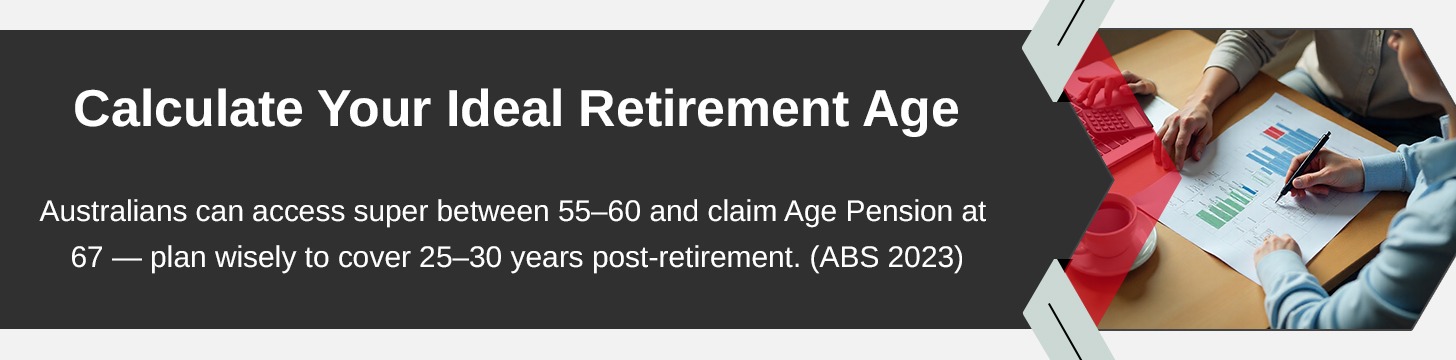

Superannuation Access (Preservation Age): Women born after 30th June 1964 can start accessing their super from age 60 once they’ve retired. (Those born before that date may have a lower “preservation age” between 55-59.)

Age Pension Eligibility: Women become eligible for the Centrelink Age Pension at age 67 (for those born on or after 1st January 1957).

Average Retirement Data (ABS 2023):

- Average female retirement age: 63.2 years

- Average male retirement age: 66.9 years

Why Women Retire Earlier?

Women often retire earlier because:

- They face career interruptions (e.g. taking time off for childcare or to care for a family member).

- They have lower super balances — the average super savings for women are around 25-30% lower than for men at retirement.

- They may rely more heavily on Age Pension support.

Tips for Women Planning for Retirement

- Have a good look at your superannuation contributions and see about doing some salary-sacrifice.

- Use co-contribution schemes and spouse contributions to boost your super balances.

- Estimate your super longevity using an online calculator (e.g. ATO or Moneysmart).

Retirement Age for Males in Australia

Like women, men can retire whenever they choose – but there are age thresholds that determine when they can access their retirement income.

| Milestone | Description | Current Age (2025) |

| Super Preservation Age | Access your super when retired | 60 years |

| Age Pension Age | Eligible for full pension | 67 years |

| Average Retirement Age | Actual retirement (ABS 2023) | 66.9 years |

Men tend to stay in the workforce longer — often because they have higher earnings, less time out for family care, or they transition to different careers later on in life.

Financial Planning Tips for Men

- Make the most of your super contributions (concessional & non-concessional).

- Consider delaying retirement to let your super grow and get a higher tax-free income.

- Diversify your assets (property, shares, bonds) to balance your post-retirement income.

Australian Retirement Age Calculator

While there isn’t a single “official” government retirement age calculator, you can get a rough idea of your ideal retirement point by taking into account:

Your Super Preservation Age:

- 55-60 years depending on your birth year.

- You can access your super once you’ve reached that age and are retired.

Your Age Pension Age:

At the moment this is 67 for anyone born on or after 1st January 1957.

Your Life Expectancy:

- ABS 2023 data: Women 85 years, Men 81 years.

- Which means your savings might need to last 25-30 years after retirement.

Your Super Balance & Lifestyle Goals:

- A modest retirement for singles costs around $32,000 per year.

- A comfortable retirement costs around $51,000 per year (ASFA 2024).

Try the Moneysmart Superannuation Calculator to model your retirement age, income and longevity.

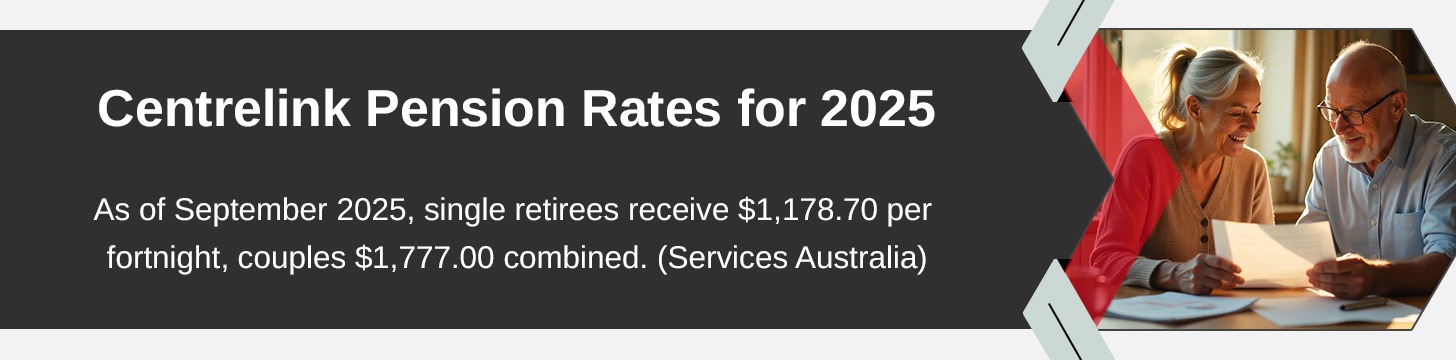

How Much Is the Full Centrelink Age Pension?

The Age Pension provides a vital safety net for retirees who meet age, residency, income & asset requirements.

As of September (indexed March & September 2025):

| Category | Fortnightly Payment | Annual Equivalent |

| Single | $1,178.70 | $30,646 |

| Couple (combined) | $1,777.00 | $46,202 |

Eligibility Rules

- You’ve got to be at least 67 years old – that’s anyone born after 1 January 1957.

- You’ve got to pass the income and assets tests.

- You’ve got to have been an Aussie resident for at least 10 years.

Pension Supplements

But that’s not all – eligible pensioners can also get:

- Energy Supplement

- Rent Assistance

- Pension Supplement

- Utilities Allowances

Check out Services Australia – Age Pension for the latest rates.

Understanding Superannuation in Australia

Super is the backbone of retirement income for Aussies. It’s a tax-advantaged savings system where your employer chucks in a slice of your salary to a fund that grows over time.

Super 101 – What You Need to Know

- Super Guarantee (SG) Rate is now 11% – and it’s going up to 12% by 2026.

- your Preservation Age is 60, unless you were born after 30 June 1964 – then it’s 65.

- you can access your super when you hit 60 and retire, or at 65 regardless of whether you’re working or not.

Your Super Options

- Accumulation Funds – Your balance grows with contributions and investment returns.

- Defined Benefit Funds – The amount you get is based on your salary and years of service (mostly for older public sector workers).

Boosting Your Super Before You Retire

- Concessional Contributions: You can put pre-tax money into your super (that’s employer SG + salary sacrifice up to $30,000 per year).

- Non-Concessional Contributions : After-tax top-ups of up to $120,000 per year.

- Government Co-Contribution: Low-income earners can get up to $500 extra from the government.

Your Super Withdrawal Options at Retirement

When you finally get your hands on your super, you can:

- Take it as a lump sum, or

- Start a retirement income stream (pension), or

- Do a bit of both for flexibility.

Why Super Matters

- super often gives you a higher and more stable income than the Age Pension on its own.

- The average super balance at retirement is around $360,000 for blokes and $290,000 for sheilas.

- Having a good super plan can help you stay financially independent for 10-15 years longer than relying on Centrelink alone.

Retirement Planning 101 – A Summary of Your Options

| Factor | Women | Men |

| Average Retirement Age | 63.2 years | 66.9 years |

| Super Access | 60 years | 60 years |

| Pension Eligibility | 67 years | 67 years |

| Average Super Balance | ~$290k | ~$360k |

| Life Expectancy | 85 years | 81 years |

Conclusion – The Future of Retirement in Australia

Aussie retirement is getting more flexible, fair, and future-focused. Now, while 67 is still the official Age Pension age, there’s a growing interest in voluntary and phased retirement that recognises the diversity of health, careers and personal goals.

Planning ahead with super optimisation, pension timing and investment diversification can turn your later years from “getting by” to living well.

Whether you’re 40 or 60 – it’s time to:

- Check how your super is going and whether your investment strategy is on track.

- Have a play with an Australian retirement calculator to model your retirement.

- Get a handle on your Centrelink entitlements.

- And most importantly – plan for 30 years of financial independence.

Frequently Asked Questions (FAQs)

1. How Much Money Can I Have in the Bank and Still Get the Full Age Pension?

There’s no fixed “bank-balance” threshold by itself — eligibility for the full Age Pension (via Services Australia / Centrelink) depends on your total assessable assets and income.

- Under the assets test, for a single homeowner, you can have up to $321,500 in assessable assets and still qualify for the full rate pension.

- For a single non-homeowner, the full-asset threshold is about $579,500.

- For a couple combined (homeowners) the threshold is about $481,500.

So, how much “in the bank” you can have depends on what other assets you hold (super, shares, property, etc.) and whether you own your home. The home (your principal residence) is typically exempt from the assets test when you are still living in it.

2. How Do I Maximise My Centrelink Age Pension?

Here are several strategies to help increase the chance of getting a higher pension rate. These must be considered carefully and ideally with your financial adviser (because individual circumstances vary):

- Keep your assessable assets under the asset-free threshold for a full pension (see Q1 above).

- Manage your income test exposure. For example, for a single person the fortnightly income limit before pension is affected is $218 (approx. $5,668 per year) as of July 2025.

- Use the Work Bonus scheme if you continue to work while on pension: you may earn more without reducing your pension. For example, new pensioners may receive a one-off credit of $4,000 to their Work Bonus income bank.

- Increase non-assessable assets like your home (which is generally exempt) rather than holding all savings in bank accounts or investments that are assessable.

- Review giftings, prepaid funeral expenses, home renovations (legal) to reduce assessable assets, though these approaches require care due to Centrelink rules around gifts.

3. What is the “2 Year Rule” for Aged Care?

When you enter a care situation (e.g. a residential aged care facility) and move out of your home, the home may remain exempt from the assets test for Age Pension purposes for a 2 year period. After that the home may be treated as an assessable asset. (guides.dss.gov.au)

Key points:

- The “care situation” includes entry into residential care, hospital, etc.

- If you leave your home to enter care and your partner remains at home, the exemption continues while the partner remains.

- After 2 years the home’s value will be included in the asset test which can reduce or stop your Age Pension.

4. What is the Maximum Income to Qualify for the Age Pension?

Under the income test for the Age Pension:

- For a single person, the fortnightly income free area (where the full pension is not reduced) is $218 as at 1 July 2025.

- For a couple combined, the income free area is $380 per fortnight.

If your income is above these amounts, your pension is reduced according to the taper rates.

For example, for singles one dollar of income above the threshold reduces the pension by about 50 cents (depending on the source).

5. What is the “$4,000 Centrelink Payment”?

This is the one-off credit under the Work Bonus scheme for new pensioners: when you start claiming an eligible payment for the first time (and meet the other conditions), you may get a one-off $4,000 credit to your Work Bonus income bank. The Work Bonus scheme allows working pensioners to earn more before their pension is reduced.